In the last few years, national parties across Europe, as well as NGOs, have called for a so-called ‘sin tax’ on meat. PETA this year urged the UK’s Chancellor: “it is time for meat and dairy to take their place alongside tobacco, alcohol, sugar, and fuel”. But why should meat – or indeed any of these purchases – be taxed?

Popes Taxing Prostitutes: for the Love of God!

The use of sin taxes dates millennia. During 11th Century Rome, Pope Clement II taxed prostitute’s half of their property sales and; some 68 popes later, Pope Leo X taxed thousands of prostitutes for their practice, using the revenues to fund religious projects. The promised bargain was, presumably, the cleansing of the sinner’s soul; a real tithe-for-tat.

Other sin taxes have been discontinued: Peter the Great’s ‘beard tax’ in 17th and 18th Century Russia, ‘window taxes’ in France, Britain and Ireland during the 18th and 19th Century, and a 20th Century ‘bachelor tax’ in Italy. All were behaviours or purchases considered undesirable in some way.

Taxes that remain today include those on alcohol, tobacco, sugar, prostitution, pornography, drugs, and gambling. Their consumption is deemed to be counter to the public interest yet seemingly impossible to eradicate. They may be addictive (gambling, for instance), highly demanded (sugar), impossible to control (drugs) or culturally re-enforced (prostitution, in particular, is referred to as the ‘oldest profession’).

Meat consumption shares the characteristics of other ‘sins’. It is highly demanded, its consumption is culturally re-enforced, and it is perceived to be immoral on a number of accounts: animal welfare, human health and the environment (in particular, the climate).

What are the reasons to tax sin in the first place, and could they justify a meat tax?

Four Reasons to Tax Sins

1. Sin taxes stifle excessive consumption

In excess, the consumption of certain goods harm consumers. Behaviours such as gambling are inherently self-destructive and the overconsumption of goods such as sugar can cause severe health problems. Sin taxes serve to stifle excess consumption and therefore alleviate the harm caused. This seems equitable insofar the burden of the tax only affects those that themselves benefit from consuming less.

In just the same way the World Health Organisation (WHO) formed a consensus around the dangers of tobacco consumption, and then sugar, so too have they formed consensus around meat consumption: in 2015, a report by IARC – the cancer agency of WHO – classified processed meat consumption (including ham, bacon and sausages) alongside tobacco as ‘definitively cancerous’ (red meat consumption was considered ‘probably carcinogenic’). Meta-analyses have also associated meat consumption with obesity and type-2 diabetes. If we tax gambling or sugar for the sake of the consumer, it might then make sense to tax meat.

Libertarians recoil at this justification for taxation. For them, it is a form of paternalism – or, ‘nanny statism’ – to control the habits of people in this way. Using taxing to manipulate consumers violates their agency; even the right to their own body. Regardless of whether consumption is healthy, this is a choice consumers ought to be free to make; in other words, they have a right be unhealthy.

These objections seem pronounced – purchasing a taxed product is, after all, voluntary. Yet taxing meat on account of its potential effect consumer health seems to discriminate against certain lifestyle choices. The meat-tax-payers might well ask themselves why the couch potatoes, sexual abstainers, nocturnals and screen addicts are going scot-free. Too little exercise, too infrequent sex or sleep, and too much time in front of a screen are all behaviours that have been associated with poor health.

If the goal is to stifle excessive consumption, a blanket meat tax is also hardly equitable. The casual meat eater should not pay for the overconsumption of the excessive meat eater. Nor should the consumer of lean white meat or fish be charged at the same rate as the consumer of (excessively carcinogenic) processed meat. This problem belies other sin taxes: should young, and casual, drinkers and smokers, whom hardly endanger themselves, be taxed the same rates as old, and binge, smokers and drinkers?

There is also a practical concern: driving the price up on meat may encourage the consumption of lower-quality meat products. This is the case with other sin taxes; most notably with tobacco, where studies show a rise in illicit cigarettes on the market following taxes on tobacco. If a reason to apply a sin tax is to protect consumers, for their own sake, taxing meat threatens the reverse effect.

2. Sin taxes reclaim costs of consumption

Sinning can be costly not merely to the sinner themselves but to their society. Taxes sins, so the argument goes, is a fair means to balancing the books. When sinners indulge in risky behaviour – smoking, drinking and overeating – eventually society must foot the bill to treat heart disease, cancers and diabetes. It is only equitable, on this account, that those who voluntarily take part in risky activities should pay for the healthcare costs that their activity causes the need for.

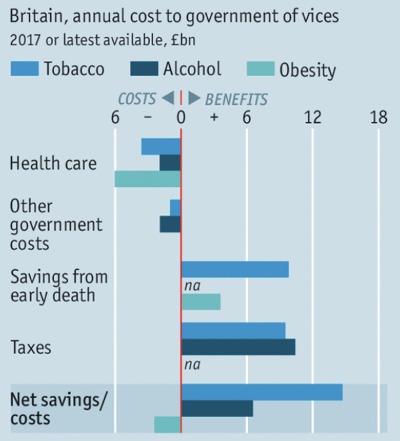

There is also another practical concern here: how to measure the true costs of consumption. Research from the Institute of Economic Affairs finds that taxing alcohol in fact brings far more benefit to the UK government than would be equitable (whereby costs are proportionate to use). Remarkably, tobacco consumption is a net benefit to the UK government’s purse even before tax is applied (thanks to the grim savings from smokers dying sooner). If the reason to tax these goods is to balance the books in society, ought we to instead reimburse smokers for their sacrifice?

It could instead be said that meat consumption is costly not to this society, but to the next. Owing to its significant contribution to GHG emissions (and climate change, more broadly), the consumption of meat is likely to cause immense costs in the future. Contemporary consumers of meat should pay for their benefiting from foreseeable costs.

One concern here: simply paying to benefit from environmentally damaging consumption threatens to normalise the behaviour and corrupt the social values that are necessary to motivate mitigation. It is also not clear how the concept of equity could apply to intergenerational costs – how could a system of taxation include the unborn?

Taxing sins to reclaim costs is problematic. It relies on a proper account of societal costs and individual contributions, which is especially difficult when the costs are intergenerational. This account also excludes the societal benefits that may be attributable to the joys of sinning, which would be difficult to square.

3. Sin taxes discourage immoral consumption

Some view sin taxes as a reflection public values and a suitable retribution for those that fail to uphold them. One reason to tax sins, then, is to signal, and reduce, the prevalence of immorality in society: a fee for vice.

Take prostitution, for instance. In the backdrop of religious hegemony, prostitution was widely viewed as a violation of the ethical principles of (Judeo-Christian) religion. Such attitudes towards prostitution persist today. Its consumption is not harmful to individual consumer, per se, but rather harmful to the moral standing of the society.

Consuming meat is considered immoral primarily because it involves indirectly causing an animal to die. This has been argued as wrong from a number of angles including an animal-rights-based perspective, an animal-interests-based account and a utilitarian perspective (indeed, the utilitarian Peter Singer explicitly advocates a 50% tax on meat for ethical reasons).

Although the consumption of sin goods, and sinful behaviours, is perceived to be immoral in some way, this is disputed in every case. A survey by Ipsos MORI estimates that 5% of the world refrain from eating meat and data from the UK suggests only a quarter are refraining from eating meat for ethical reasons. If the goal is to discourage immoral consumption, is it plausible to suggest that eating meat is – yet – considered immoral?

Such moral estimations depend upon a given society and vary over time. Beards are no longer seen as a sign of vanity in Russia (if not elsewhere), singletons in Italy are no longer viewed as taxably offensive, and traditional sins of prostitution and (some) drugs are increasingly legitimised or otherwise considered acceptable in society. Using sin taxes to discourage immoral consumption may be to impose it as unanimously immoral.

A more agreeable stance: it is not wrong per se to consume animals; it is instead the manner of the process. There is much to be said, ethically, about the difference between farming home-grown chickens and those intensively farmed – the latter described by animal welfare expert John Webster as “the single most severe, systematic example of man’s inhumanity to another sentient animal”. The most realistic possibility for consensus here is to suggest that intensively farming animals causes disproportionate harm, and this practice is, in a more universally agreeable sense, immoral.

In this case, however, a meat tax would be counter-productive to its very purpose. Such a tax would encourage farmers to farm more efficiency and intensively. High efficiency farming leads to poorer animal welfare by incentivising worse conditions, the slaughtering of a greater number of smaller animals, and the manipulation of animal genetics.

More generally, the idea of taxing certain goods and services on account of their perceived immorality is troubling. Behaviours that are truly immoral (and uncontroversially so) should be prohibited, not charged. Allowing the market to underwrite moral values may establish a licence to behave immorally, should it be affordable.

4. Sin taxes fund moral venture

Sin taxes can effectively serve the primordial function of taxes: to raise revenue. Sin taxes are easy to collect, generally popular, and lucrative. This reason to tax sins is indiscriminate to the morality of the consumption itself, focusing instead on the benefit of taxes to government’s ability to spend on moral venture.

This is a common, if not merely political, justification for imposing sin taxes. In Colorado, the tax on marijuana consumption is raised specifically for moral ventures: to fund schools and youth consumption prevention programmes. Costa Rica’s climate levy on gasoline is used to fight climate change by compensating landowners for reforestation efforts.

But such loose earmarking for revenue projects might be little more than a deceptive illusion. If the promised expenditure, associated with the tax, does not lead to a real increase in budget spending, then the earmarking is illusionary: the moral venture comes at the price of forgoing another cause.

Even if the earmarking leads to a genuine increase in spending, it is hardly equitable for one group in society – here, the sinners – to fund moral ventures to the benefit of the rest. This is especially unfair given that sin taxes are highly regressive: the less well-off are both more likely to consume sin goods and services, and consume a disproportionate amount. What kind of society funds their moral venture through taxing those with the least ability to pay?

Taxing Meat: A Sin Tax Error

Part of the problem with taxing meat is Pigouvian; specifically, a contradiction that arises when appealing to both the immorality of the behaviour and the beneficial source of revenue. The following two statements seem at odds:

(i) A meat tax should be implemented to raise revenue.

(ii) Meat consumption is wrong and should be discouraged.

If meat consumption is discouraged, it will no longer be useful as a source of revenue. If meat consumption is a source of revenue, then it relies on consumption not being discouraged.

Nevertheless, the consumption of meat causes great harm both to this society and the next. When deciding to curb it, governments should look elsewhere in the policy arsenal.

Positive information campaigns, or ‘suasion’, can help nudge consumers away from meat. This does not necessarily offend the agency of consumers; indeed, studies in the UK reveal over two-thirds of consumers want to consume more sustainably – they are just unaware of how to do so. Those that wish to buy ‘greener’ products, for instance, rely on inappropriate heuristics such a ‘food miles’ to guide their food choices (even long-distance foods expend only 11% of their total carbon footprint on transport).

Widening consumers ‘choice architecture’ through better food labelling, ‘meat-free’ days, and mandatory availability of meat-free options could all provide better incentives. One obstacle, however, is that powerful industry actors affect consumer’s choices in precisely the opposite way. A study from the Behaviour Economics Team shows an impressive marketing effort from the UK’s Pork Lobby in 2006 that increased consumption by some 21,900% in six years.

Price, rather than information, is the compelling determinant of food choice. Governments currently deliver immense subsidies to the animal agriculture sector; the total within OECD ‘club of rich countries’ is $52 billion – which is higher than the GDP of three of the club’s members. These subsidies drive the price of meat below what it costs society, and prices consumers out of buying alternatives. A considered withdrawal of meat subsidies – perhaps providing instead to healthier, more sustainable, and less cruel alternatives – could prove the most effective and ethically justified tool available.